Glossary of the finance and accounting

bookkeeping

Bookkeeping is the process of recording financial transactions in the books of a business (= accounting records). It is also a term used as an abbreviation for double-entry bookkeeping, a particular form of bookkeeping.

accounting

Accounting is a process which identifies, organises, classifies, records, summarises amd communicates information about economic events, usually, but not exclusively, in monetary terms. Bookkeeping is often considered as being included within accounting, but accounting is a much wider concept than bookkeeping, as accounting may also be regarded as a transformative process as it turns the raw data recorded in the bookkeeping process into useful information.

reporting

Reporting is the communication aspect of accounting. It involves providing information about a business to interested parties, such as owners and managers, and is usually achieved by the production of management information in the form of management accounts or financial statements (income statement, balance sheet and cash flow statement).

account

A section of a book or ledger in which a business entity will record transactions of the same kind, e.g, sales of goods of the same type. In the context of double-entry bookkeeping, an account will often mean a T-account.

double-entry bookkeeping

This is a method of recording a business's transactions/events in a set of T-accounts, such that every transaction/event has a dual aspect and needs to be recorded in at least two T-accounts. It was devised over five hundred years ago, and first written about by an Italian monk called Luca Pacioli. It is now the most commonly used method of bookkeeping.

bookkeeper

A person employed to maintain the books of a business (= accounting records) and keep them up to date.

posting

A term used to mean recording transactions/events in T-accounts.

balance

A balance is the amount of the difference between the debit and credit sides of a T-account. It is inserted on the side with the lower total, and is the figure, which, when included, makes the total of both sides the same. If the insertion occurs on the debit side, it means that total credits have exceeded total debits. Balances on certain asset, liability and capital accounts may be carried forward (or down) to the next accounting period. If, for example, a debit balances arises on such a T-account, it is carried forward to the credit side.

trial balance

A list of the balances extracted from all the individual accounts in an entity's accounting records, showing all debit balances in a left-hand column and all credit balances in a right-hand column. If the underlying double-entry bookkeeping has been done correctly, the totals of both columns should be the same.

balancing off

This is the practice of summing the debit and credit sides of a T-account and inserting a missing figure (a balance) to make both sides equal. It is usually done at the end of an accounting period.

accounting period

An accounting period (sometimes also referred to as a financial period, period of account or accounting reference period) is a period of time for which a business prepares financial results. The accounting period can be any length of time, and the length may be determined by the reason financial results are required, for example, providing management with information (often monthly or quarterly), or producing a set of financial statements. The latter is usually done annually, though this may vary when a business is set up, ceases, or changes its accounting period end date.

period of account

An accounting period (sometimes also referred to as a financial period, period of account or accounting reference period) is a period of time for which a business prepares financial results. The accounting period can be any length of time, and the length may be determined by the reason financial results are required, for example, providing management with information (often monthly or quarterly), or producing a set of financial statements. The latter is usually done annually, though this may vary when a business is set up, ceases, or changes its accounting period end date.

accounting reference date

This is the date at the end of an accounting (reference) period, most usually the date in a year up to which an entity prepares its financial statements. It is also referred to as a closing date. UK business entities may choose any date in the year as the end of their annual accounting period, but this is not always the case elsewhere in the world.

closing date

This is the date at the end of an accounting (reference) period, most usually the date in a year up to which an entity prepares its financial statements. It is also referred to as a closing date. UK business entities may choose any date in the year as the end of their annual accounting period, but this is not always the case elsewhere in the world.

income statement

This is one of the main components of a set of financial statements. It shows the total costs deducted from total income to calculate the profit or loss for an entity over a financial period. It was formerly commonly referred to as a profit and loss statement/account.

profit and loss statement/account

This is one of the main components of a set of financial statements. It shows the total costs deducted from total income to calculate the profit or loss for an entity over a financial period. It was formerly commonly referred to as a profit and loss statement/account.

statement of financial position

A statement of the total assets and liabilities of an entity at a particular date, usually the last day of the entity's accounting period. Total assets will always equal total liabilities, but there are various ways in which information can be presented. Often a balance sheet is regarded as being a 'snapshot' of assets and liabilities at the balance sheet date. International Accounting Standard 1 uses statement of financial position as a term for a balance sheet.

financial statements

A set of statements summarising an entity's financial activities over a given period, usually a year. They generally comprise an income statement (previously called a profit and loss account/statement), a balance sheet and, if required, a cash flow statement, all with supporting notes. Companies must provide additional statements.

set of accounts

A term used to refer to financial statements (themselves often referred to as a set of financial statements), that is, the income statement and balance sheet, and commonly the cash flow statement as well.

International Accounting Standards Board (IASB)

This was set up in 2001 as the successor to the International Accounting Standards Committee. It is an independent, privately funded body which takes responsibility for developing, improving and promoting the use of international accounting standards, with a particular aim to bring about convergence of national standards with international ones.

International Accounting Standards (IASs)

Any of the accounting standards issued by the International Accounting Standards Committee (IASC) between 1973 and 2001, at which date the IASC was superseded by the International Accounting Standards Board (IASB), which adopted all the IASs in issue, but advised that its own standards when issued would be known as International Financial Reporting Standards (IFRSs).

International Financial Reporting Standards (IFRSs)

Any of the accounting standards issued by the International Accounting Standards Board (IASB).

management information system (MIS)

This is a system within a business which provides information needed to manage that business effectively and support the managers' decision making process. A significant characteristic of an MIS is that it analyses other information systems within the business, for example, those applied in operational activities, accounting, etc.

accounting information system (AIS)

This is a system which processes accounting data and turns them into useful information, such as income statements and balance sheets at the end of an accounting period, or the management accounts which are typically produced monthly to help managers monitor and control business activities and make decisions. It is often referred to as an accounting system (for short). The term is also commonly used to refer to the computer software a business may use for accounting and bookkeeping purposes.

accounting system

Information is data processed for a purpose. Once data have been processed into information, that information can be used to aid decision making, which will additionally require the exercise of judgement. Meaningful decisions cannot be taken on the basis of data alone.

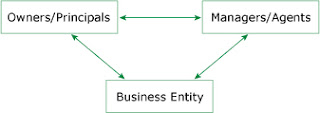

agents

An agent (sometimes referred to as a steward) is a person appointed by another person, called a principal, to act on the principal's behalf. Directors of a company act as agents of the shareholders (principals). An accountant may also act as an agent on behalf of shareholders in his/her capacity as auditor, or when acting as a tax adviser to a client in dealing with HM Revenue & Customs.

stakeholders

All those who have an interest in an organisation. They may be users of, or persons with a varying degree of interest in, an entity's financial statements and dependent on or influenced by its financial performance.

external auditor

An independent, external person or firm appointed formally by shareholders to write a report to them on the externally reported financial results of the company in which the shareholders own shares.

internal auditors

An internal auditor is appointed by a entity itself to carry out checks, for example, that internal controls within an organisation are operating satisfactorily or that the entity is complying with legislation, such as that pertaining to health and safety. He/she is often a member of an internal audit department within an entity and will report to an internal committee, rather than being appointed by and reporting to shareholders.

turnover

A term used not only to refer to the actual selling of goods/services to customers, but also to the income or revenue derived therefrom (also referred to as revenue, sales revenue, sales turnover and turnover).

costs

A cost is expenditure on goods and services required to carry out the operations of an entity. Sometimes costs which are not directly involved in generating sales are referred to as expenses or overheads, but these terms are often used interchangeably without distinction of meaning, especially in non-accounting contexts.

profit

In an income statement, when total costs are deducted from total income, if there is an excess of total income over total costs, then this is referred to as a profit (sometimes also called a surplus, especially if the entity concerned does not have a profit making motive, e.g., if it is a charity).

loss

In an income statement, where total costs exceed total income, a loss arises (often referred to as a deficit by non-profit-making entities). A loss can also arise, for example, on the disposal of individual non-current assets, if they are disposed of for less than their net book value (= cost/value less accumulated depreciation to the date of disposal). Such a loss is often referred to as a capital loss.

assets

The International Accounting Standard Board (IASB) defines assets as resources controlled by a business as a result of past events and from which future economic benefits are expected to flow. They might be things a business owns, such as the machinery it uses to manufacture goods or vehicles it uses to deliver goods to customers.

liabilities

The International Accounting Standards Board (IASB) defines liabilities as present obligations of a business arising from past events, the settlement of which is expected to result in an outflow from the business embodying economic benefits. They might be sums of money owed, for example, to lenders who have loaned money to a business or to suppliers of raw materials for manufacturing purchased on credit.

plant

This is the equipment needed to operate a business. It is often used in the phrase 'plant and machinery' as a general term to include all types of apparatus and equipment, but there is no distinct dividing line between what is plant and what is machinery.

non-current assets

Non-current assets are assets for long-term use, generally speaking, for more than one year. Capital expenditures that have been capitalised (i.e. recognised in the balance sheet) appear on the face of the balance sheet as non-current assets.

tangible assets

A type of non-current assets, which have physical form and can be touched (the latter being the basic meaning of tangible), for example, machinery, vehicles, etc.

intangible assets

The word tangible means something that can be touched. In terms of assets, a tangible asset is an asset that has physical form. An intangible asset therefore does not have physical form and cannot be touched, though the existence of many kinds of intangible assets (e.g., copyrights, patents and trademarks) may be evidenced by some form of documentation. This is not the case with goodwill, however, which is probably the most intangible of all assets.

patents

A patent is the grant of an exclusive right (usually to an inventor or an inventor's employer) to exploit an invention.

copyrights

A copyright confers an exclusive legal right to reproduce, or permit others to reproduce, literary, dramatic, artistic or musical works (e.g., recordings).

trademarks

A trademark (a type of intangible asset) is a mark that uniquely identifies a trader's particular goods or services. It can take the form of a mark, symbol, device or word(s), individually or in combination. In the UK, a trader (manufacturer, dealer, importer, retailer or service provider) may register a trademark at the Register of Trade Marks (held at the Patent office), which will allow the trader exclusive use of the trademark, initially for seven years. Provided that the trademark has been properly used, and will continue to be so used, registration is then renewable.

inventory

This is the international accounting terminology to denote trading stock, and may comprise raw materials, work in progress (partly finished items) or finished goods.

current assets

Current assets include cash, liquid assets (also called cash equivalents, which can be converted into cash within a maximum of three months), and assets that are normally converted into cash within the course of business or within one year.

work in progress

This typically refers to inventory items which are partly completed. As manufacturing processes are often continous, not all items will be finished and ready for sale at the end of an accounting period.

trade receivables

Receivables or trade receivables are sums owed by customers to whom a business has sold goods or services. It is the international accounting term now used for trade debtors.

owner’s interest

This is money, resources or assets put into the business by owners, and also referred to as owner's interest or equity. Capital can also mean other things, for example, in economic theory, physical capital (machinery) or financial capital (money).

non-current liabilities

This is the international accounting term now used to refer to long-term liabilities. These are sums owed which are due for payment more than a year after the end of an accounting period.

current liabilities

These are amounts owed by a business to others which are payable within one year or less at the end of an accounting period. There are several different types of items which could be included in current liabilities, but trade payables, accruals and short-term loans are common examples.

horizontal format

A format used to present a balance sheet in which all the assets listed on the left-hand side and all the liabilities (and capital) are listed on the right-hand side.

vertical format

A format used to present a balance sheet in which assets are shown in the top half and capital and liabilities in the bottom half. The net assets approach to a balance sheet is a variant vertical format, whereby current and/or long-term liabilities are deducted from assets to derive a net assets figure equal to the total capital shown in the bottom half.

net assets approach

This is one possible approach to formatting a vertical balance sheet. The top half shows assets less liabilities to derive the figure for net assets, which is then the same as the total capital shown in the bottom half. Opinion varies as to whether non-current (long-term) liabilities should be treated as capital and so not deducted in deriving the figure for net assets, or whether they are part of the liabilities and therefore deductible.

international accounting approach

This refers to the terminology, format, presentation and disclosure to be applied in preparation of specified company financial statements consequent on the adoption of International Accounting Standards (IASs) and International Financial Reporting Standards (IFRSs) issued by the International Accounting Standards Board (IASB).

drawings

These are resources (usually in the form of cash or goods) taken out of the business by the proprietor of an unincorporated business or partners in a partnership. An example might be when a sole proprietor takes some of his/her inventory for personal use or pays a personal bill through the business bank account.

cash flow statement

This is a statement which shows the inflows and outflows of cash and cash equivalents (investments easily convertible to known amounts of cash, usually within a three month period) over a business's financial period. International Accounting Standard 1 specifies a particular format and headings for company cash flow statements.

notes to the financial statements

Financial statements (income statement, balance sheet and cash flow statement) are usually accompanied by a set of notes to the financial statements, disclosing additional financial information, explanation and analyses, which are more conveniently shown separately from the main statements, or are required to be shown in notes to comply with accounting standards, etc.

Trade payables

Payables or trade payables are sums of money owed to persons or entities who/which have supplied goods or services to a business. It is the international accounting term now used for trade creditors.

Reactions

Posted by ARVIND ENTERPRISES GROUP

CareerBro - Your Career Guidance Partner

India's best career counseling and guidance platform for students and professionals. Unlock your full potential with CareerBro's expert advice.

Learn More

%20_%20Logos%20_%20Design%20Bundles.jpg)

.jpg)

- ARVIND ENTERPRISES GROUP

- Arvind Enterprise Group is conglomerate and the group of holding company works in foods,transport,education,medical industry . real estate, construction, consultancy, business ,capitals,e-commerce ,energy,automobiles technologies,finance,artificial Intelligence and many other sectors|

%20_%20Logos%20_%20Design%20Bundles.jpg)

.jpg)

what is Bookkeeping?

Bookkeeping is the process of recording transactions in the financial records of a busine…

what is Accounting and reporting?

Accounting is a process which identifies, organises, classifies, records, summarises and …

Series Funding: A, B, and C

A startup with a brilliant business idea is aiming to get its operations up and running…

moving money forward over multiple years

it is future value that moves money forward across four time periods .moving money forwar…

Startup Capital Definition, Types, and Risks

What Is Startup Capital? The term startup capital refers to the money raised by a new…

Top 30 Investing Principal's.

In This Blog We Understanding 30 Investing Principal's. 1. Diversification: Investin…

Distribution of returns - Graphical representation

So when we talk about allocating our wealth into different financial assets, there are…

The balance sheet

At the end of an accounting period, all assets and liabilities are listed from individual…

%20_%20Logos%20_%20Design%20Bundles.jpg)

How we adapt the the process of the investment

Arvind capitals process for investing is a easy they focus on the long-term profitabi…

%20_%20Logos%20_%20Design%20Bundles.jpg)

Investment Management in the New Era: Strategies for 2023 and Beyond

Investment Management in the New Era: Strategies for 2023 and Beyond *Introduction:* The…

%20_%20Logos%20_%20Design%20Bundles.jpg)

Arvind capitals is a assets management company. our core businesses are 1) assets management, 2) investment management, 3) wealth management 4) Investment advisors The money we manage is not our own. It belongs to many people – in many different locations – all trying to achieve their most important financial goals.-Arvind capitals

0 Comments