Accounting is a process which identifies, organises, classifies, records, summarises and communicates information about economic events, usually, but not exclusively, in monetary terms. While accounting is often considered as including bookkeeping as well, it is much wider than bookkeeping. It may also be regarded as a transformative process in that it turns the raw data recorded in bookkeeping into useful information. Data lack meaning until they have been processed into meaningful information. What good is it to know that a book cost a bookshop £10? Those data will only become information when they are combined with something else that enables you to assess them within a relevant context, such as how much the book would have cost had the bookshop bought it from a different supplier or how much profit the bookshop made when it sold the book to a customer.

The communication aspect of accounting involves the reporting of information about a business to interested parties, such as owners and managers. Results of all transactions over a period of time need to be summarised, presented and interpreted in order to assess a business’s performance and its financial position at a given date. The period of time for which results are calculated is referred to as an accounting period or period of account . An accounting period can be any length of time, and the length may be determined by the reason for which a set of results is required, for example, to provide management with information, to support an application for a bank loan, etc. Commonly, however, an accounting period is of a year’s duration, and however often businesses produce sets of results, they will always produce an annual set of results, as these are required for specific purposes, such as for taxation or, in the case of companies, filing with a regulatory authority. Only in certain well defined circumstances will sets of results for periods other than a year be accepted for these specific purposes. For example, the first accounting period for companies in the UK must be more than six months, but no more than 18 months.

The date on which an annual accounting period ends is referred to as the business’s accounting reference date or closing date . For UK business entities, this date can be any date in the year and does not have to coincide with a calendar year, though this is not necessarily the case elsewhere. The form in which results are presented is usually twofold: a calculation of the business’s overall profit or loss for its accounting period, referred to as an income statement or profit and loss statement/account ; and a statement of financial position as at the end of the accounting period, also called a balance sheet. In this course we will use the terms ‘income statement’ and ‘balance sheet’. The income statement and balance sheet together are often referred to as the financial statements or set of accounts.

Different accounting terminology

The different names for the different parts of financial statements have arisen as a result of different customs, rules and regulations over the years, when we look especially at the impact of the International Accounting Standards Board (IASB) and the introduction of International Accounting Standards (IASs) and International Financial Reporting Standards (IFRSs) . ‘Profit and loss account’ was for many years a common term, but it was felt to be less than precise, particularly when, for example, it was used by entities which did not have a profit motive, such as charities. IAS 1, the international accounting standard which deals with the presentation of financial statements, therefore, introduced the term ‘income statement’, which can be more universally applied. At the same time, it suggested the replacement of another, much older term, ‘balance sheet’, by the term ‘statement of financial position’. IAS 1, however, did not make adoption of the new terms mandatory. ‘Income statement’ has been widely adopted, but not ‘statement of financial position’. While many professional accounting training manuals use the latter, it is not yet widely used by businesses, which still continue to use the term ‘balance sheet’. In this course, we therefore use the terms ‘income statement’ and ‘balance sheet’. In addition to widespread use, the term ‘balance sheet’ is also useful when learning accounting as it helps remind you that a balance sheet itself should ‘balance’, that is, both halves/sides should add up to the same figure, and that certain individual account balances will be included there.

Although businesses produce formal income statements and balance sheets for, and at the end of, accounting periods, they can do so at any time, and often produce them more regularly to help managers monitor and control business activities and make decisions, as mentioned above. This adds further dimensions to accounting, as it helps look to the future, rather than focusing on transactions that have already occurred, and in this sense accounting has a management function, as a part or sub-set of the wider management information system (MIS) of a business. In this context, accounting is sometimes referred to as an accounting information system (AIS) or in short, accounting system .

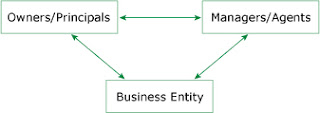

Stewardship

Persons who run or manage businesses are not always those who have invested money and/or resources in the business. They manage money and/or resources which are owned by others, and act as stewards (or agents ) on behalf of owners (sometimes called principals ). The concept of stewardship places an obligation on stewards to provide financial information relating to the resources which they control, but do not own.

%20_%20Logos%20_%20Design%20Bundles.jpg)

%20_%20Logos%20_%20Design%20Bundles.jpg)

%20_%20Logos%20_%20Design%20Bundles.jpg)

%20_%20Logos%20_%20Design%20Bundles.jpg)

.jpg)

.jpg)

{kind=link}

0 Comments